This article was first published by MPUG on 22nd December, 2015.

***

Internal Rate of Return (IRR) is a project selection technique that takes a comparative approach for selection. When you're taking the PMI® PMP® exam, you should expect questions on IRR. In your day-to-day life as well you can check with IRR to help make better decisions, such as whether to buy insurance. Hence, IRR is a useful concept to know.

To understand IRR, you first have to understand net present value (NPV). NPV, as the name suggests, tells the net or total present value of cash flow for a project. Any project will encompass investment, which is considered cash outflow. Also, a project is undertaken to give the organization certain value back, which are cash inflows.

The formula for NPV is:

NPV = Present value (PV) of cash inflows (positive) + present value (PV) of cash outflows (negative)

- If NPV is positive, that's good. You can consider the project for selection.

- If NPV is negative, it's bad. The project shouldn't be considered for selection.

I. The Definition of IRR

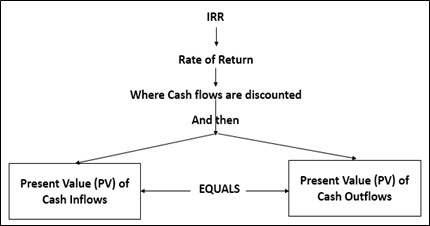

Internal rate of return is the interest rate (or discount rate) at which the net present value for the project is zero.

In other words, the rate at which cash inflows equal cash outflows is considered as internal rate of return. It's called "internal rate of return," because there are no other external influences or environmental factors.

As the cash inflows equal cash outflows, for IRR the NPV for the project will be zero. If we put it mathematically, the equation would be:

NPV = 0

=> PV of cash inflows for the project (positive) + PV of cash outflows for the project (negative) = 0

=> PV cash inflows for the project = PV cash outflows for the project

The rate at which present value of cash inflows equals PV of cash outflows will be the IRR. IRR is always noted in percentage terms. To understand, let's look at an example.

An Example of IRR

Your organization has an investment of $100,000 for a project. After one year you will get $110,000 in return. Calculate the IRR.

Present value (PV) of cash outflows for the project = $100,000

Future Value (FV) of cash inflows for the project = $110,000

It's called future value, because we'll get the money after one year.

Therefore, PV of cash inflows for the project = $110,000/(1+R), where R is the rate of return or discounted rate.

For IRR, the value of NPV is zero.

=>PV of cash inflows = PV cash outflows

=> $110,000/(1+R) = $100,000

=> 1 + R = $110,000/$100,000

=> R = ($110,000/$100,000) - 1 = $10,000/$100,000 = 1/10

Or R in percentage terms = (1/10) * 100 = 10%

The IRR for the project is 10 percent.

Let's say you've received the capital of $100,000 at a rate of 12 percent from the investor. After all, someone -- internal or external -- will need to invest in the project. That investor will be expecting a return out of it. This rate is called Cost of Capital (CoC) in accounting terms, because there's a cost associated with it. You have to provide a return for this capital.

However, as you found out above, your IRR is coming at 10 percent, while your CoC is at 12 percent. Will you go for the project? Obviously not. You wouldn't be making any money out of it by executing this project. This leads us to an important conclusion in project selection while using IRR.

- If IRR is greater than the desired cut-off rate (or CoC), then you will go ahead with the project.

- If IRR is less than the desired cutoff rate (or CoC), then you won't proceed.

II. Ways to Calculate IRR

IRR can be calculated in two ways: for uniform cash flows and for non-uniform cash flows.

II.1: IRR Calculation for Uniform Cash Flows

In the previous example, I showed a simple project with a one-time investment. However, for uniform cash inflows -- a series of cash flows that's uniform year after year, IRR is calculated considering the annuity discount factor.

The formula for annuity discount factor is:

Project investment = Annual net cash flow * Annuity discount factor

=>Annuity discount factor = Project investment/Annual net cash flow

Annuity is a fixed sum of money to be paid every year as a series of payments. (This is another accounting term.)

Once the annuity discount factor is calculated, annuity table is referred to find IRR. Annuity tables are available on accounting sites. If this topic surfaces on your exam, it'll probably reference the present value of annuity factors.

Example 2: Annuity Factors

For this example, I've modified the first example. You have a $100,000 investment for a project. After one year you expect $110,000 in return. Find out the IRR with the help of the annuity factor.

The annuity factor table is given below.

In this case, there is one-time investment and a return is mentioned for one year. I have put that into a table as shown below. Note that cash inflows are mentioned as positive, whereas cash outflows are negative, highlighted in red and put in parentheses.

Annuity discount factor = Project investment/Annual net cash flow

=> Annuity discount factor = $100,000/$110,000

=> Annuity discount factor = 10/11 = 0.9090 = 0.9091(approx.)

Looking at the above annuity discount factor table (given in the question), we have a rate of 10 percent for an annuity factor of 0.9091. So the IRR for this project is 10 percent.

Now, let us change this example a bit, to examine annual uniform cash flow.

Example 3: Annual Uniform Cash Flow

You have a $100,000 investment for a project. The expected return on the project in its useful life is $125,000. The useful life of the project is five years. The cash inflow is expected to be uniform. Find out the IRR. The annuity table is shown below.

Here, the cash flow is uniform. Considering the cash inflows and cash outflows, we have the following table. As we have $125,000 over a period of five years, for each year the cash inflow will be $25,000. Note that cash inflows are mentioned as positive, whereas cash outflows (investment) are negative.

Hence, Annuity Discount Factor = Project Investment/Annual Net Cash flow

= $100,000/$25,000

= 100/25 = 4, which is close to 3.9927.

For the annuity discount factor of 3.9927, looking up the table shown in the question, the rate comes out to be at 8 percent. Hence IRR for the project is 8%.

II.2: IRR Calculation for Non-uniform Cash Flows

For non-uniform or uneven cash flow, we have to calculate the IRR in a different way. First, we need to find out the average cash flow in a year, from which we derive the annuity discount factor. Then, looking up the annuity table, we get an approximate value of IRR. From there, by trial and error and interpolation, the final IRR is derived.

In an uneven cash flow scenario, the formula for IRR is:

It doesn't matter if you have NPV or PV in the denominator. The final value of IRR will remain the same. Both formulas above are correct for IRR.

It's unlikely that you'll have questions about this in the PMP exam. But I've put the formula in in case you're wondering what happens if there's uneven cash flow.

III. IRR for Mutually Exclusive Projects

IRR can be used to make selection decision between two or more independent projects. The general rule followed for IRR: The higher the better. In other words, all other things being equal, the project with the highest IRR should be selected. Let's take another example to understand this concept.

Example 4: Choosing Between Projects based on IRR

There are four projects before the selection committee, out of which only one can be selected. The IRR for each project is shown below. Which one will be chosen?

Answer:

The project with the highest IRR will be chosen. Above, that’s project B with an IRR of 42 percent.

However, there’s a note of caution when mutually exclusive projects are involved. If both NPV and IRR are present, it’s a good idea to look for NPV as well. A project with higher IRR but lower NPV wouldn’t be preferable over a project with a lower IRR but higher NPV.

To illustrate, here’s an example.

Example 5: IRR and NPV

There two projects, A and B, with the following cash flows. The discount rate is at 10 percent. Which project should be selected?

For project A, NPV = - $1,000 + $2,100 = $1,100

For project A, we have to make NPV zero to find out IRR.

=> - $1,000 + [($2,100)/(1+IRR)] = 0

=> 1 + IRR = 2,100/1,000 = 2.1 => IRR = 2.1 – 1 = 1.1

=> IRR = 110%

Above, I have applied the simple formula, as outlined before, to calculate the IRR. I can also look at the annuity table to derive the IRR.

For project B, NPV = - $10,000 + $15,000 = $5,000

For project B, we have to make NPV zero to find out IRR.

=> - $10,000 + [($15,000)/(1+IRR)] = 0

=> 1 + IRR = 15,000/10,000 = 1.5 => IRR = 1.5 – 1 = 0.5

=> IRR = 50%

Now, which one to choose?

• Project A higher IRR (110%), but lower NPV ($1,100)

• Project B lower IRR (50%), but higher NPV ($5,000)

Project B will be selected as it gives maximum value to the stakeholders or has higher wealth maximization.

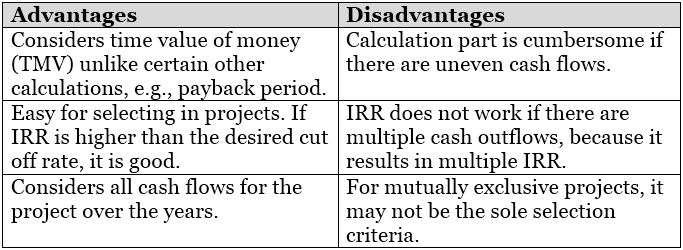

Finally, let us look at the advantages and disadvantages of IRR to have needed understanding on it for the PMP exam.

IV. Advantages and Disadvantages for IRR:

Nice article. If you need more on Finance Assignments you can visit this article.

ReplyDeleteHi Satya,

ReplyDeleteVery good article. Thanks for explaining IRR.

I have come across one question from Scordo test book.

Your company is considering buying a building worth $1 million. If the company buys this building and rents it out for the next five years, it will get $100,000 per year as rent (receivable by the end of each year). At the end of the fifth year, the company will resell the building at $1.1 million. What is the NPV of this?

A. 62092

B. 600000

C. 1600000

D. 2200000

Answer and explanation from book :

A - NPV = discounted inflows – discounted outflows Since the full investment, i.e. $1 million, needs to be made now, we don't have to discount the outflows. However, we need to discount all the inflows by 10% per annum. The discount formula is: Present Value (PV) = Future Value / (1 + discount rate)^period For year 1: PV1 = 100,000 / 1.1^1 = 90,909 For year 2: PV1 = 100,000 / 1.1^2 = 82,645 For year 3: PV1 = 100,000 / 1.1^3 = 75,131 For year 4: PV1 = 100,000 / 1.1^4 = 68,301 For year 5: PV1 = 1,200,000 / 1.1^5 = 745,106 Hence the total PV of the inflows = 1,062,092 NPV = 1,062,092 – 1,000,000 = $62,092 [PMBOK 5th edition, Pages 195, 198]

Big question I have here is: where/why is that 10% discount is applied if is not on the question or any references in the PMBOK guide to any related assumptions!!!???

Just wondering if for discount rate they have used IRR (Internal rate of Return).If yes, can you pls explain how. Have they considered that company is going to sell it for $1.1 million only after 5 years. Meantime they will be having some cash inflow for 5 years. When calculating IRR, have the considered this?

Thanks for your help.

Regards

Kavita